Scheduled Maintenance

Scheduled maintenance will be performed on the server in the near future.

We apologize in advance if the site becomes temporarily unavailable.

Celní válka neprospívá nikomu, je přesvědčen český prezident Petr Pavel. Je mu líto, že Spojené státy v otázce cel volí nátlakový přístup, když stačilo jednat. Pokud bylo cílem ukázat, že síla si svoje protlačí sama, pak to samozřejmě nesvědčí spojeneckým vztahům, řekl dnes prezident českým novinářům v mauritánském Nuakšottu, kde je na dvoudenní návštěvě.

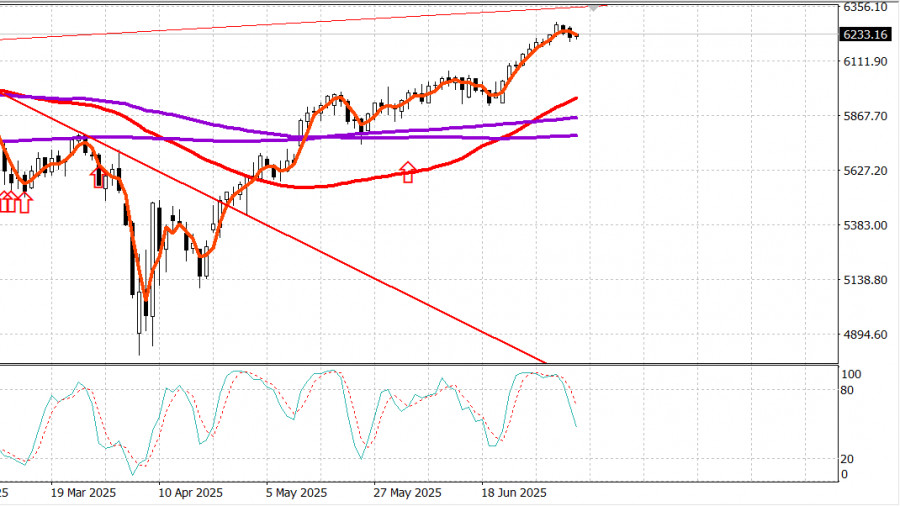

S&P 500

Overview for July 8

US market pulls back on Trump tariffs

Major US indices on Monday: Dow -0.9%, NASDAQ -0.9%, S&P 500 -0.8%, S&P 500: 6,230, trading range: 5,900-6,400.

The stock market headed into the holiday weekend enjoying a fireworks display that included stronger-than-expected June jobs data, some excitement over the potential passage of Trump's "One Big Beautiful Bill," and record highs in both the S&P 500 and Nasdaq Composite.

However, this upside momentum fizzled out yesterday as part of a typical post-rally correction, amid the news cycle offering a convenient excuse for selling.

Specifically, President Trump began sending letters to a select group of countries, warning that higher tariff rates will take effect starting August 1 if better trade terms for the US are not reached by then. The EU was not included in this group. Japan and South Korea were the most prominent countries named, each facing a 25% tariff rate. At the same time, Trump extended the negotiation deadline on tariffs from July 9 to August 1.

This news should not have come as a surprise, given earlier reporting on the issue. Nevertheless, it served as a clear catalyst for Monday's broad-based and orderly sell-off.

The S&P 500 traded down, sliding to the 6,200 area, before trimming losses in the final 90 minutes of the session.

The Philadelphia Semiconductor Index (-1.9%) and the Russell 2000 (-1.6%), two of the recent standout gainers, ranked among the biggest losers on Tuesday.

The advance-decline line favored decliners by nearly 4 to 1 on the NYSE and nearly 3 to 1 on the Nasdaq, reflecting a market where losers were in clear abundance.

Nine of the 11 S&P 500 sectors closed in negative territory.

The two exceptions were defensive-oriented utilities (+0.2%) and consumer staples (+0.1%).

The weakest performer was the consumer discretionary sector (-1.3%), dragged lower by a steep drop in Tesla shares (TSLA 294.11, -21.24, -6.74%).

The decline followed concerns that Elon Musk may be too distracted by his new political initiative, the "Party of America," and a Wall Street Journal report that Tesla is facing intensifying competition in China.

Other sectors posting the worst performance included materials (-1.0%), energy (-1.0%), financials (-1.0%), communication services (-0.9%), and healthcare (-0.9%).

Energy stocks were pressured by disappointing second-quarter guidance from Shell plc (SHEL 69.84, -2.08, -2.89%) and OPEC+'s decision to increase output in August by 548,000 barrels per day, up from 411,000 in July.

WTI crude futures, however, ended the day up 1.5% at $67.96 per barrel.

Separately, Treasury bonds closed their session with losses across the curve. Long-term bonds posted the largest declines, resulting in a curve steepening that some interpret as concern that inflation will linger at elevated levels and the Fed has no plans to cut interest rates.

The yield on the 2-year note rose by one basis point to 3.89%, while the 10-year yield climbed four basis points to 4.39%.

There were no major US economic data releases yesterday.

Year-to-date:

S&P 500: +5.9%Nasdaq: +5.7%DJIA: +4.5%S&P 400: +1.2%Russell 2000: -0.7%

Energy: Brent crude at $69.20 — up about $1 on the day. Oil is currently shrugging off the OPEC+ production hike.

Conclusion: We may be seeing the beginning of a correction in the US market. We recommend going long if the S&P 500 declines to around 6,000, or about 4% below current levels.

Scheduled maintenance will be performed on the server in the near future.

We apologize in advance if the site becomes temporarily unavailable.

コンタクトする

コンタクトする