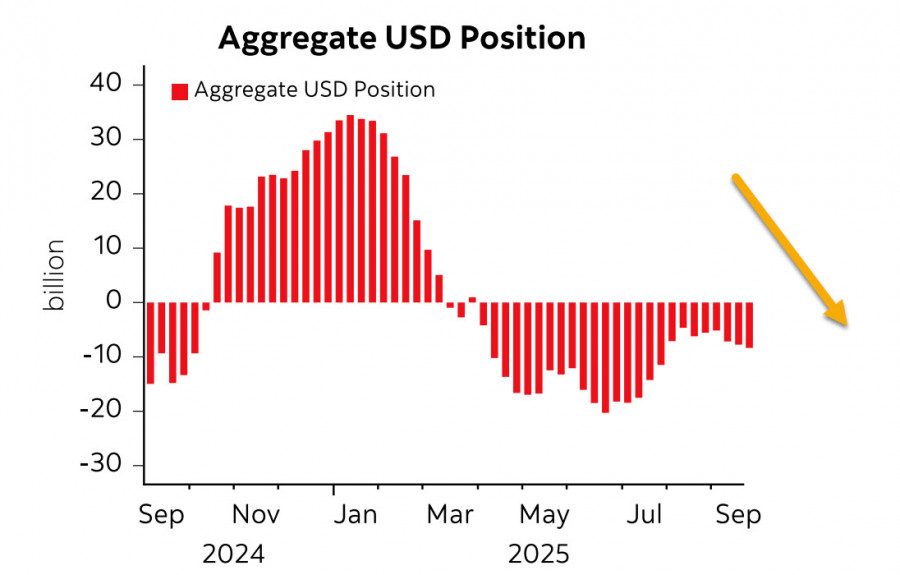

According to the latest CFTC report, the aggregate short position on the U.S. dollar against major world currencies increased by $0.8 billion over the reporting week, reaching -$8.6 billion. Speculative positioning on the dollar remains bearish. At the same time, a noticeable shift was recorded only in the yen (+$1.5 billion), while changes in other currencies were minimal, indicating that the trend toward a weaker dollar has not strengthened and currently looks more neutral.

U.S. GDP growth in Q2 was revised upward from 3.3% to 3.8%, suggesting that, by growth measures alone, the U.S. economy appears to be in excellent condition. However, two indicators raise questions about these figures.

The first is job creation. In a growing economy, new jobs are typically created at above-average rates; however, this trend has been disproven in recent months. While 158,000 new jobs were created in April, only 19,000 were added in May, and 13,000 were lost in June. The average monthly growth of just 54,700 is far too low to justify such strong GDP growth. Including July and August data, the increase in new jobs fell to around 30,000 in recent months. Declines have been seen across all sectors, raising alarm among many Federal Reserve members. Unemployment has changed little, but this reflects tighter immigration policies, which have significantly reduced the labor supply, keeping unemployment artificially stable.

The second indicator is inflation. The index rose by 0.26% in August (vs. 0.13% in July). There is no slowdown, and since most new tariffs took effect in August, their impact will be reflected in consumer prices in October–November.

Until recently, the market was pricing in four rate cuts next year. However, as of Monday, the outlook shifted: while an October cut is seen as virtually inevitable (with about a 90% probability), the next one may not occur until December or March. Overall, markets still expect four cuts through the end of 2026, but rate expectations have turned more bullish for the dollar.

The balance is precarious: a weakening labor market and looming recession argue for rate cuts, but inflation risks remain elevated. With most central banks also cutting rates amid still-high inflation, such actions may increase risks rather than reduce them.

Friday's September employment report is in jeopardy: if Congress fails to pass a budget bill on Tuesday, the government could shut down by Wednesday. If Nonfarm Payrolls are not released on Friday, markets could be paralyzed by uncertainty, losing a key benchmark for forecasts.

With liquidity shortages rising sharply, funding sources must be found. Launching a new wave of QE in a high-inflation environment is highly unlikely—impossible, as long as Powell chairs the Fed. Foreign inflows are unlikely, either, given elevated tariffs. That leaves domestic reserves as the only option.

The source of such reserves becomes clear when examining the dynamics of the stock market. The S&P 500 continues to set record after record, with the 6840 target nearing. However, this milestone may never be reached, as a reversal could begin earlier.

We anticipate a significant correction in equity indexes, which could occur at any moment. The nearest target is 6340, and in the event of a deeper crisis, a rapid decline toward 6150 cannot be ruled out.

The dollar still looks weak, but this weakness may soon come to an end. Signs of a bullish reversal are becoming increasingly evident.

আমাদের সাথে যোগাযোগ করুন

আমাদের সাথে যোগাযোগ করুন