Dovish expectations and market sentiment have been growing—but is this truly the case? In recent weeks, nearly every Federal Reserve official has spoken publicly. Now, during the pre-meeting "blackout period" (with the next Fed meeting just a week away), market participants have a relatively clear sense of what to expect from the U.S. central bank. The prevailing assumption is that the Fed has adopted an increasingly dovish stance, especially in light of a supposedly "cooling" labor market. This analysis aims to challenge that assumption.

To begin with, it's important to note that only a few Fed officials have expressed openly dovish rhetoric—namely, those closely aligned with President Donald Trump. Steven Miran, Michelle Bowman, and Christopher Waller were all appointed by the current president, and Trump is still considered a contender for Jerome Powell's soon-to-be-vacant position. It's no real surprise that this trio appears willing to vote in favor of lowering interest rates in support of Trump's agenda.

However, voting alone is not enough. Each of these officials has justified their stance by arguing that the labor market is cooling too quickly and that monetary policy should therefore be eased sooner. On the surface, this claim seems plausible—but the data tells a different story.

Due to the recent government shutdown, the most critical labor reports—namely, Non-Farm Payrolls and the unemployment rate—were not released for September. Only the ADP private payrolls report was published, and it is widely considered an unreliable reflection of official labor market conditions. Therefore, we lack solid evidence to conclusively state that the labor market is continuing to weaken.

It's also worth mentioning that only three out of twelve voting members of the FOMC consistently favor rate cuts at each meeting. The others have indicated a willingness to ease policy only if there is clear evidence of sustained labor market weakness. Moreover, nine committee members continue to focus on inflation risks. Should the Consumer Price Index continue to rise, these members may abandon support for further monetary easing.

Based on all of this, the Fed's next moves will hinge on incoming economic data. If the data does not support further action, then the Fed may hold rates steady. In short, the so-called "shift toward dovish sentiment within the FOMC" is largely a myth. Any growing dovish bias is limited primarily to Miran, Bowman, and Waller.

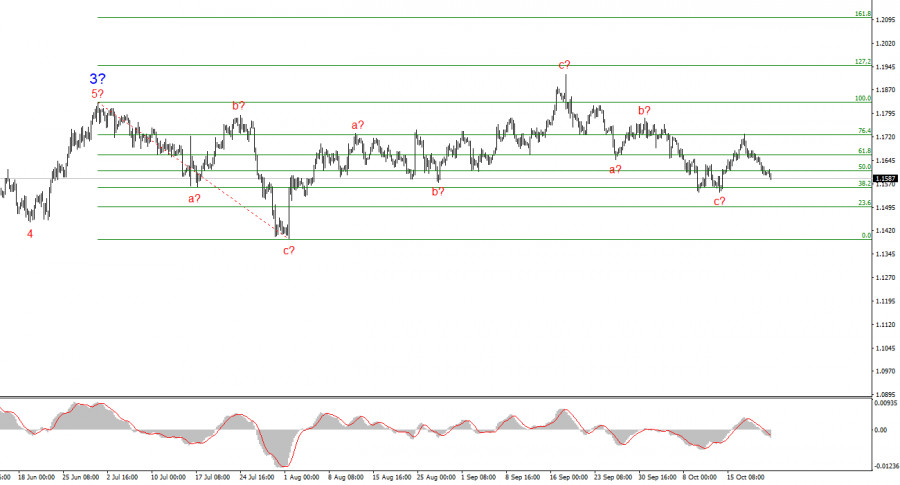

Based on the current wave analysis of EUR/USD, the pair continues to build an upward segment of the trend. The wave structure remains heavily dependent on news related to President Trump's decisions, as well as the foreign and domestic policy direction of the new U.S. administration. The current upward trend may extend up to the 1.25 area. At this moment, we are likely observing the formation of corrective wave 4, which is nearing completion and appears to be complex and extended. Therefore, I remain focused on buying opportunities. By year-end, I expect the euro to rise toward the 1.2245 level—approximately the 200.0% Fibonacci.

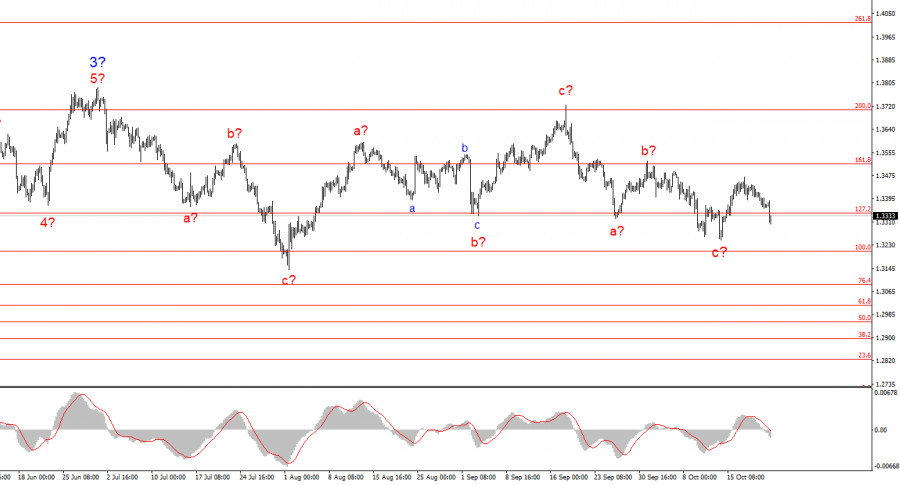

The wave pattern in GBP/USD has evolved. We are still within an upward, impulsive segment of the trend, but the internal structure has become more complex. Wave 4 is taking the form of a three-wave correction and is proving substantially more drawn out than wave 2. The most recent three-wave bearish correction appears to be completed. If this assessment is correct, the upward movement within the broader wave structure may resume, with initial targets near the 1.38 and 1.40 figures.

ລິ້ງດ່ວນ

ຕິດຕໍ່ພວກເຮົາ

ຕິດຕໍ່ພວກເຮົາ