MEXICO CITY (Reuters) – Akcie mexického výrobce cementu Cemex v pondělí posílily, protože prodej aktiv v Dominikánské republice pomohl společnosti téměř ztrojnásobit čistý zisk v prvních třech měsících roku 2025, a to i přesto, že společnost oznámila meziroční pokles základního zisku.

Akcie společnosti Cemex vzrostly v dopoledním obchodování o 4,5 % a staly se tak nejvýkonnějšími akciemi na hlavním mexickém akciovém indexu poté, co společnost oznámila zisk za první čtvrtletí ve výši 734 milionů dolarů, což představuje nárůst o 189 % díky prodeji aktiv v Dominikánské republice.

Společnost Cemex uvedla, že 618 milionů dolarů z jejího čistého zisku za čtvrtletí pochází z ukončených činností.

Zároveň oznámila 18% pokles zisku před úroky, daněmi, odpisy a amortizací na 601 milionů dolarů, což je v souladu s odhady LSEG, a to kvůli slabšímu pesu a poklesu objemů na domácím trhu, uvedla ve zprávě.

There's no defense against a crowbar—except another crowbar. The return of financial markets to a world ruled by raw power has pushed EUR/USD below 1.17. Geopolitical risks continue to plague the Eurozone economy. They create uncertainty, and rising oil prices are particularly unwelcome for a region that imports most of its "black gold." Add to this the threat of snap elections in France, and the drop in the main currency pair ahead of US inflation data seemed logical. However, the US PPI data dampened the mood for the US dollar.

If Moscow is not prepared to sit down at the negotiation table with Kyiv, Washington is ready for economic war. For this, it needs the support of Brussels, but the EU has been unable to get Hungary and Slovakia to act in unison. If they succeed, then secondary sanctions on China and India, for their support of the armed conflict in Ukraine, will become a reality.

Essentially, this means oil prices are likely to rise, since Russia is one of the world's largest suppliers. A supply restriction is a direct path to a Brent rally. For the Eurozone, which is heavily dependent on imported oil, this is bad news. Unsurprisingly, speculators began to unwind short positions on the US dollar, leading to the decline in EUR/USD.

On top of that, Israel delivered a surprise strike on Qatar targeting Hamas leaders. This was a bolt from the blue for the Middle East and pushed oil prices even higher.

Add to this the interception of Russian drones by Poland and Poland's subsequent request to NATO for a coordinated response, and it becomes clear that Europe remains a dangerous and troubled region. If money is fleeing the US due to Donald Trump's antics, in the EU, geopolitics continues to set the tone.

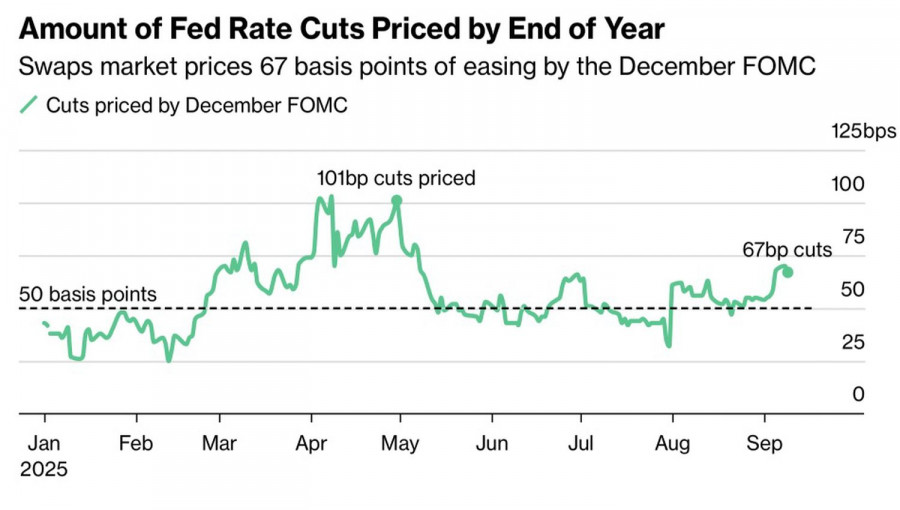

Against this backdrop, investors seemed to have forgotten that they were selling the US dollar because of a weakening labor market and the rising likelihood of the Fed resuming its monetary easing cycle in September. The futures market is currently pricing in 65 basis points of monetary expansion by the end of the year.

If investors have forgotten anything, the inflation data reminded them about the US dollar's vulnerability. Producer prices slipped into negative territory in August, which was music to the ears of EUR/USD bulls. Slowing PPI and CPI figures give the Fed more leeway for aggressive monetary expansion. However, nobody knows what the final consumer price figures will look like yet.

Thus, geopolitics is currently battling central banks, and so far, politics is winning out at least for now.

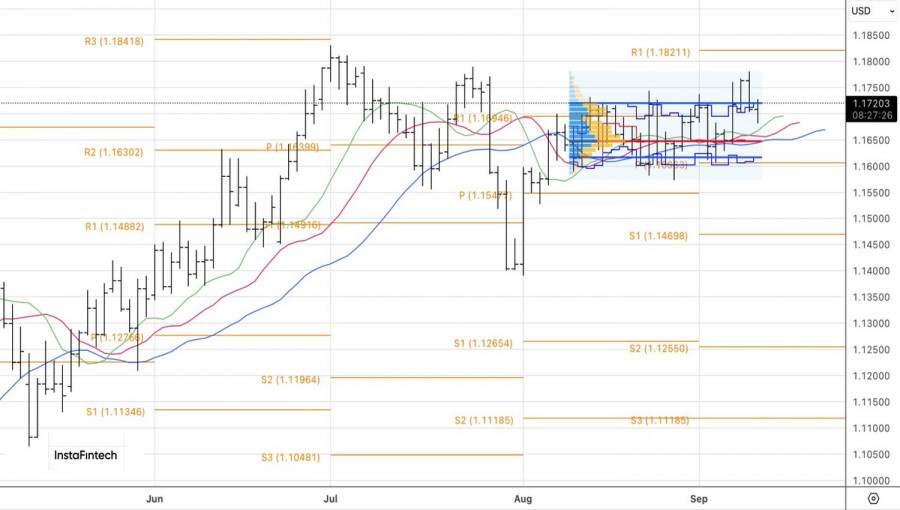

Technically, on the daily chart for EUR/USD, much depends on how the current bar closes. A close below the upper boundary of the fair value range at 1.1615-1.1715 will strengthen the risk of returning to consolidation. A rise above 1.1715 would be a signal to buy euros against the US dollar—especially if a pin bar forms.

ລິ້ງດ່ວນ

ຕິດຕໍ່ພວກເຮົາ

ຕິດຕໍ່ພວກເຮົາ